.png?width=63&height=51&name=logo%20(6).png "logo (6)")

Benefits of KYC

- Understanding your clients: By verifying customers, companies have a better understanding of their clients’ financial profiles.

- Risk assessment: This helps companies assess the risk involved before entering into a business deal.

- Long-term relationship: Companies can make informed decisions regarding the suitability of clients and what it might take to maintain a business relationship with them.

- Builds mutual trust: KYC ensures a greater level of trust and transparency between both parties.

- Regulatory compliance: KYC processes are modular, so they can easily be expanded with add-ons or security checks to fit the required guidelines. It is a small investment that ensures your company and its clients remain safe.

On a broad scale, KYC is also beneficial for customers. These regulations are in place to prevent criminal acts, such as terrorist financing; thereby ensuring that wider markets and economies remain safe.

KYC Process

The KYC process is generally comprised of 6 steps:

- 1. Data collection

- 2. Document checks

- 3. Information validation

- 4. Risk assessment

- 5. Client approval

- 6. Ongoing monitoring and record maintenance

There are several different KYC programs that can be implemented. Choosing the right one is a critical decision. Unsuitable KYC programs can lead to non-compliance penalties. The appropriate selection is dependent upon the type of organization.

Customer Identification Program (CIP)

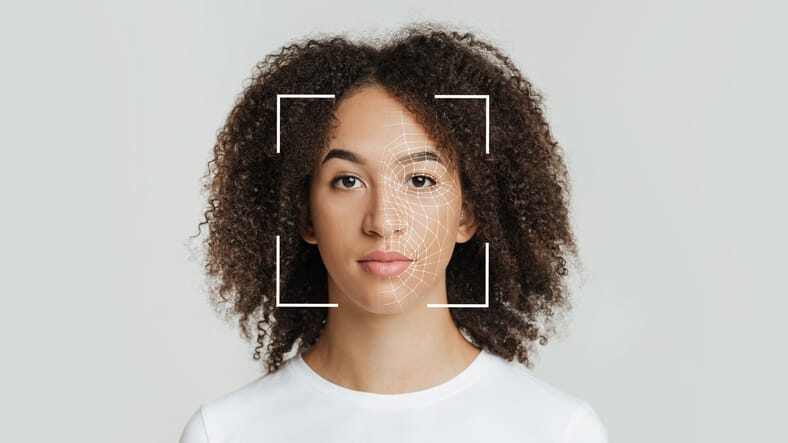

The Customer Identification Programme is the most important component of the KYC framework: the verification of a customer's identity. In order to prevent spoofing and ensure that the customer is who they say they are, each individual or legal entity must be verified. In the case of the latter, the beneficial owners must be verified.

Customer identification includes, but is not limited to, data collection, document checks, identification and verification, sanctions list checks, etc. Documents, especially ID cards, are usually verified using a document reader and document verification software.

Customer Due Diligence (CDD)

CDD collects additional client information to assess the individual's risk factor. This information enables you to make an informed decision about a potential client. It also ensures that the information is reliable and comes from a valid source.

Higher-risk clients typically require more rigorous identification checks, which can take significantly longer.

Enhanced Due Diligence (EDD) / Continuous Monitoring

Once a customer has passed the initial screening, their activity and status will continue to be monitored. This may include: transactions, sanctions lists and media coverage. The scope and frequency of EDD will depend on the risk profile of the customer.

In order to maintain a KYC-compliant relationship, EDD keeps customer profiles under constant review.

Record Maintenance

Keeping records of the initial KYC process and ongoing transactions is an important step.

This will ensure that you will be able to identify any illegal activity that may occur in the future. If you come across any illegal transactions, terrorist funding, etc., it must be reported immediately to the relevant authorities.

It is recommended that you keep customer records for at least 5 years.

Reporting

If suspicious activity occurs, it should be reported immediately. Having a set of procedures in place will enable you to deal with the situation quickly with the appropriate authority.

KYC Requirements

KYC has a general set of requirements along with country specific regulations. Moreover, these basic requirements differ from industry to industry – the financial industry being the strictest among them.

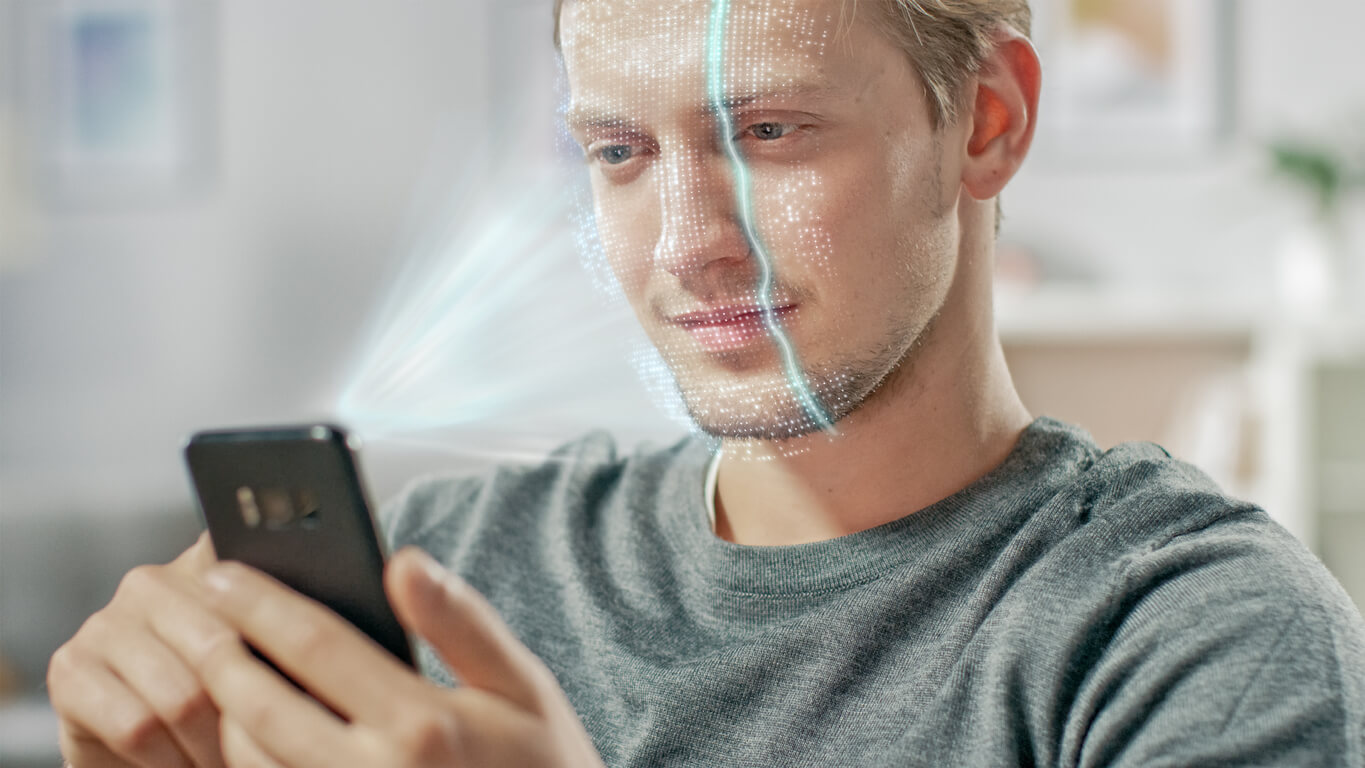

- Facial verification – facial verification ensures the live presence of the individual (to quickly and effectively identify spoof attacks).

- Document verification – document verification ensures that the government-issued ID is neither forged, invalid, nor faulty. It is common for institutions to request more than one form of ID (i.e. birth certificate, social security card, passport, driver’s license, etc.) to confirm the customer’s identity.

- Address verification - address verificiation validates the address on government-issued identification docments against Proof of Address (POA).

Examples in Europe:

- Germany: The Federal Financial Supervisory Authority (BaFin)

- Switzerland: Financial Market Supervisory Authority (FINMA)

- Italy: Banca d’Italia

- United Kingdom: The Money Laundering Regulations

Examples in other countries:

- US: Financial Crimes Enforcement Network (FinCEN)

- Canada: The Financial Transactions and Reports Analysis Centre of Canada (FINTRAC)

- Australia: Australian Transaction Reports and Analysis Centre (AUSTRAC)

- India: Reserve Bank of India

- South Africa: The Financial Intelligence Center Act 38 (FICA)

The PXL Vision Solution

Understanding the fundamentals of KYC is the first step to making an informed decision about which identity verification solution is best for your organisation. To avoid the risk of non-compliance penalties, ineffective KYC processes and customer churn, PXL Vision has developed a fast and easy-to-use identity verification solution using state-of-the-art machine learning intelligence and AI technology. Our solution is designed to be configured to meet the specific needs of each organisation.

The PXL Vision solution

The PXL Vision solution

- Utilizes high-efficiency, precise AI technology

- Verifies customer in 30 seconds or less

- Accurately performs POI and POA checks

PXL Vision Document Checks

PXL Vision Document Checks

After full integration and custom configuration of the PXL Vision solution, customers can easily complete their eKYC checks. The general steps include

- Scan the required document(s) with a smartphone camera

- Taking a short selfie video

- Submit and complete

PXL Vision process

PXL Vision process

- Check MRZ: We pull information from the machine-readable code lines (MRZ) and run several checks on them.

- Examine the visual inspection zone (VIZ): We review the remainder of the document or VIZ.

- Assess authenticity: We run several security checks and analyze hundreds of visual key features to ensure that the document is real.

- Read biometric NFC chip, if available: This allows us to read information from the document. We also make sure to inspect the chip to confirm that it has not been tampered with.

PXL Vision offers two core identity verification solutions: PXL Ident® and PXL Pro. Our primary solution, PXL Ident®, is a user-friendly SaaS solution that can be individually adapted to local KYC regulations.

POA check

POA check

To perform a POA check, we use an API from a third party service provider. This implementation makes it possible to follow through with a POA check anywhere in the world while maintaining accordance with the KYC guidelines of your country.

.png?width=800&height=533&name=Phone_Hands_Typing%20(1).png)

Summarizing the KYC principle:

- The KYC process is an approach that is particularly suitable for banks and financial institutions

- Profiles of potential customers are examined to ensure that they do not engage in illegal activities with their open business accounts.

READ MORE More on the topic of KYC

KYC Check

Find out how PXL Vision can make the KYC check a easy for you. A secure KYC check optimises your processes and helps companies to prevent money laundering and corruption.

KYC Document

Find out what a KYC document is and how PXL Vision can verify it for you quickly, easily and securely. Discover the benefits.